MORE FREE TERM PAPERS

- RESEARCH PAPERS: - HISTORY -

|

|||||||||||||||||||

A Brief History of Tea in Nepal

Nepali tea industry owes its roots to the colonization of India by the

East India Company. Numerous tea plantations around the hill station of

Darjeeling were promoted by the British. Hybrids of tea bushes were introduced

in several districts in Nepal - Illam, Taplejung, Panchthar and Dhankuta

within a few years after their introduction in Darjeeling and the first

tea estates were established in 1863 in Illam and Jhapa. But whereas the

Darjeeling tea production soon emerged into a prosperous commercial industry,

the Nepalese tea production remained low profile until the 1990s, unable

to fulfill domestic demand.

Decades earlier, in 1966, the Nepalese government had established the

Nepal Tea Development Corporation. Initially, Nepalese tea leaves were

sold to factories in Darjeeling. With time, the Darjeeling tea bushes

had become old and along with internal changes in the industry it led

to a deteriorating quality of the Indian tea. These conditions made the

Nepalese tea leaves a valuable input for the Indian factories. During

the last decade tea processing factories have been built and turned Nepalese

tea production into a fully commercialized industry. Although, even today

some farmers sell their tea to Indian factories as they get a better prices

from across the border.

In the early 1990’s, large tea plantations run by the government mainly

dominated the tea sector. Through reforms in 1993 the state owned National

Tea Development Corporation was privatized. Its regulatory functions were

handed over to the National Tea and Coffee Development Board under the

Agricultural Ministry. To promote the industry further the government

launched a new tea sector policy at the end of 2000. This policy seeks

to ease access to credit and land for tea producers as well as building

human capacity and establish better opportunities for export promotion.

A clear priority is also set for which type of tea processing should be

promoted.

The goal of this paper is to examine the general trends in Nepalese tea

industry, in particular, the changes brought about by the privatization

in the early 1990s. The following pages will examine the two distinct

types of tea industry, Orthodox and CTC, look into Nepal’s export performance

and finally attempt to assess the impacts of liberalization on small farmers

as well as commercial tea estates.

2. The Two Types of Tea Industries

Orthodox Tea

Orthodox tea is grown in the hills of 6 districts in eastern Nepal, i.e.

Illam, Panchthar, Dhankuta, Terathum and new areas of Sindhupalchok and

Kaski. The orthodox tea production accounts for 12-15% of total tea production.

Its total production amounts to 1500 Tons and covers 6689 hectares of

cultivated land. The primary contributors are small farmers who sell their

leaves to buyers in nearby factories or to those in Darjeeling.

The climatic conditions in the Eastern hills of Nepal provide ideal conditions

for the production of high quality orthodox tea. Another advantage compared

to Darjeeling tea is that the bushes are young and produce better quality

leaves. Because of the premium price paid to orthodox tea, 96% of it is

exported while little is sold domestically mostly in souvenir packages

suited for tourists.

Present status in the orthodox industry:

Production (Mil. Kg/yr) - 1.5

Area / ha - 9775

Tea estates - 63

Small farmers - 18750

Factories - 19

Small farmers share in area - 77%

Small farmers % share in production - 67.8

Export as % of total production - 96

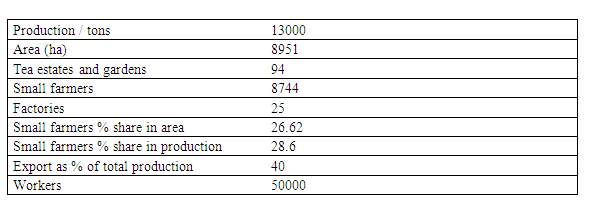

CTC Tea

CTC is produced in Terai in the district of Jhapa and covers around 90% of domestic consumption. The CTC grown in Nepal is known to be of average quality. Whereas small farmers form the backbone of the orthodox tea production, it is largely big tea estates which are behind CTC tea production. Most of the tea estates have their own processing factories and some use bought leaf factories to manufacture tea. It is estimated that around 66576 workers are employed by the tea estates as pluckers, factory workers and in other functions. Many of the daily-wage workers are landless and live at the estates on a permanent basis.

Present status of the CTC industry

In both type of industries, CTC and Orthodox, the Nepalese tea industry has undergone large expansion during the last decade and has been an important source of employment. A Tea Policy came into force in 2000, which prioritized orthodox tea production given its natural qualitative advantage. INGOs like the GTZ and WinRock are currently supporting orthodox tea promotion (marketing, branding, code of conduct and technical trainings). However, the coverage may be inadequate and there is a need for further assistance to many more farmers. The sector is facing a number of problems with inadequate infrastructure, excess use of chemicals, low-skilled labor, and a lack of well-planned strategy for upgrading the production process as well as marketing the finished good.

3. Tea Consumption Facts

The domestic Tea consumption survey has indicated the consumption of

2.42 cups in a day per person. The annual per capita consumption is 350

grams of Tea

Following table indicates the per capita consumption of Tea in different

countries.

Ireland has the highest percentage consumption (3kg) followed by UK, Turkey. Nepal stands on the last (0.35kg).

4. Nepal’s Export Performance in Tea

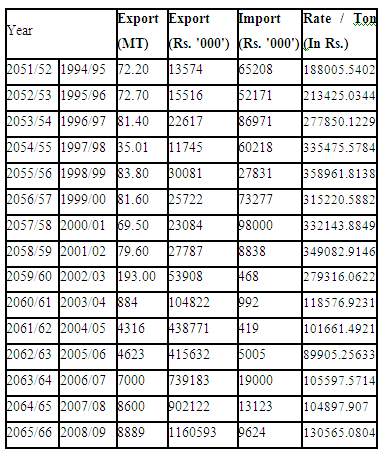

Until 2003, the volume of tea exported annually from Nepal was around

180-200 tons, after which the tea sector saw an exponential rise in exports

of more than a thousand percent, largely as a result of liberalization

carried out ten years earlier. However, the value of tea per ton was more

or less constant until 2002 when it started to decline. If one calculates

from the figures below, the value per ton in 2002 was Rs.349083 whereas

in 2004 it had declined to only Rs 118577 per ton.

Over the last 10 years, Nepal has become increasingly self reliant on

tea and import of CTC has decreased substantially. Initially the import

of CTC was meant to cover domestic demand, but has now has been substituted

by domestic production. Compared to the value of exported tea the value

of imported tea has decreased in the beginning of the 2000, but then recovered

in 2004.

Nepal’s current export performance is strong compared to other sectors.

In 2002/03,Nepal’s tea exports experienced a major uplift, from an average

annual export of around 80 tons, exports grew exponentially to 984 Mt

in 2003/04 and 4,316 Mt in 2004/05 (Table 30). Nepal has become increasingly

self-reliant on tea and the import of Cut, Tear, and Curl (CTC) tea has

decreased substantially. This massive change took place largely as a result

of liberalization carried out ten years earlier.

The major export market of Nepalese tea are Germany, Japan, France, Italy,

Hong Kong, India, Pakistan, U.K., Switzerland, Australia, Netherlands

and U.S.A. Nepal imports C.T.C to meet domestic Consumption

The export potential is high. The current export performance

is strong compared to other sectors. Nepal produces both CTC (lowland),

which is primarily for domestic consumption, and highland orthodox tea,

which is mainly exported. The tea sector experienced significant growth,

following its liberalization over a decade ago. From an average of 80Mt

exports grew to over 4,000Mt last year. The tea industry has been expanding

in recent years along with an expansion of its plantation areas from 3,5000

hectares in 1996 to 15,000 hectares in 2004. There is large potential

to expand the cultivated area. With the positive conditions in this sector,

the government has set very ambitious production targets. However, the

tea sector is unlikely to meet the targets, mainly due to problems relating

to the insurgency, the fragmentation of production, and the lack of auctioning

facility or quarantine laboratory. The world market, at the same time,

is showing its first sign of price recovery since its slump caused by

massive overproduction. Overall, Nepal has favourable market access conditions

to the most attractive markets including Japan, US, EU and Russia. Its

production of tea is, however, rather specialized in niche markets such

as highland orthodox tea and high quality and organic.

Domestic supply conditions. Nepalese tea comes in two

main categories: orthodox/green (leaf) tea and black tea/CTC tea. The

former is produced in the hills for export and is available only in limited

quantities, while the CTC tea produced in the Terai region is mostly used

for domestic consumption but some is exported to India. The last decade

or so has seen a tremendous growth in the Nepali tea industry with the

plantation area expanding from 3,500 hectares in 1996 to 15,000 hectares

in 2004. This, nearly five-fold, increase in the plantation area has been

matched by an increase in the output of tea (11,651 thousand kg in 2004

against 2,905 thousand kg in 1996). Most plantations are still young and

yet to start yielding harvest, which suggests that production is set to

increase even further. According to the government statistics, the area

under tea cultivation in 2004/05 was 15901 hectares of land and the production

in the same year was 12606 metric tons (Table 32). In 2003/04, 1.55 million

kg of orthodox tea and 10.06 million kg of CTC tea were produced. Currently,

the incremental ratio of tea production in Nepal is 20 percent per annum.

The government aims to produce 36,000 Mt of CTC tea by the year 2010-11,

from which 600 to 650 Mt will be available as surplus for export. Similarly,

the target fixed for orthodox tea production within the year 2010-11 is

set at above 16,000 Mt.

At present, tea cultivation has been extended in different districts from

Jhapa in the Terai region to Ilam, Paanchthar, Dhankuta, Terhathum, Sankhuwasabha,

Bhojpur, Dolkha, Ramechhap, Solukhumbu, Sindhupalchowk, Nuwakot, and Kaski

in western Nepal.

Despite all these favourable conditions the tea sector is unlikely to

meet its production targets.

The first, and major, constraint identified by owners of tea estates is

Nepal’s continued political instability. The situation in Nepal remains

precarious and unpredictable. This has had an adverse impact on the day-to-day

business of the tea factory owners, farmers and marketers.

Secondly, production is concentrated in a number of fragmented areas such

as gardens, factories. Consequently marketing efforts are also disjointed.

For instance, Nepal's tea factory is supplied by over 7,000 small Green

Leaf farmers spread around the agricultural areas in the hilly region.

In tea production, it is a well-known fact that 35 per cent of the quality

of tea is determined by the quality of the green leaves. The methods,

in which small farmers are engaged, are, therefore, crucial for the quality

of the final output. Even if one farmer, out of the total 7,000, uses

a harmful pesticide then the whole production can be rendered worthless.

There is, therefore, a clear need for tea producers to implement a code

of conduct to be enforced at all levels of the value chain of tea production

process.

Thirdly, the lack of a quarantine laboratory is another issue for Nepal.

Nepalese tea has to be sent to Kolkota for food testing standards, which

is costly in terms of time, money and management. Definite progress is

required on the long-standing proposal to develop a joint quarantine laboratory

or to create a mutual recognition agreement between India and Nepal.

Lastly, the lack of auction system is an issue. A market research study,

facilitated by the German aid agency GTZ in Germany revealed a number

of interesting facts about how Nepali Orthodox tea is perceived in Europe's

single largest market, Germany. The results suggested that German buyers

were not interested in tea sourced from a variety of individual gardens.

In India the issue of scale is solved by organized large-scale auctioning

of tea in Calcutta. During this process, producers provide various grades

of tea for sampling. Based on the quality of the tea international brokers

offer their prices on behalf of the international buyers. This process

is clearly missing in Nepal, where international buyers are not able to

negotiate with different buyers based on the grades of tea.

The Himalayan Tea Marketing Cooperative (HIMCOOP) has been formed to provide

a one-stop agency for tea sales. Presently, their day-to-day operations

are funded by a SNV while the marketing strategy has been structured with

the assistance of GTZ and WINROCK International. The cooperative is actively

participating in the tea world exhibitions from America to Europe, and

agencies such as GTZ and WINROCK International along with the government

are co-operating to promote the brand image. HIMCOOP has appointed Mr.

Reinhold Messner, the famous mountaineer, as a Brand Ambassador of Nepali

tea in Europe. HIMCOOP is branding Nepal tea in the international market

as “Quality from the Himalayas”. A distinctive logo has been designed

for Nepali tea and was unfurled at the Tea and Coffee World Cup organized

in Hamburg in September 2005.

The government has been actively supporting the industry. The Government

of Nepal introduced the National Tea Policy in 2000 with the goal of increasing

the production of tea through the increased participation of the private

sector in the tea cultivation. The government grants a number of incentives

to the tea industry.

Competitiveness prospects are favorable.

- There is large potential in terms of expanding the area under cultivation.

- There is a need to improve transparency in marketing, quality, costs

and prices by the implementation of an auction system. This is reflected

in the number of stakeholders who, during interviews, stressed the value

of a tea auction facility in Nepal. One advantage of an auction facility

is that it can redistribute a higher share of the final price of tea to

farmers. At present, the farmers' share is estimated to be about 45% of

the price of manufactured tea and about 29% of the export price. Tea growers,

and some manufacturers, stress that they ought to get higher shares of

the final prices. A competitive and transparent auction system and better

infrastructure for small holders will help to increase the shares.

- Competitive markets, quality products and agreements made through the

WTO are major challenges to the Nepalese tea stakeholders. If these challenges

were properly addressed and were responded to with policy initiatives,

in line with improving world markets, the future of tea industry in Nepal

would be very favourable.

5. The current socio-economic impact in terms of employment is high.

The job creation impact of this sector is very high compared to other

sectors. This sector seems to be a strong engine for farmer’s income generation

and poverty reduction as orthodox Tea gives higher returns compared to

other crops. This sector is also likely to have a high impact on total

employment compared to other sectors - especially female employment- as

estimates suggest that it already accounts for around 105,000 people.

Priority actions

- Establish testing and certifying agencies under joint public- private

partnership.

- Set-up R&D facilities for further quality improvement and productivity

growth

- Set-up facilities to improve the tea auctioning process in Nepal in

order to improve transparency in marketing, quality and prices

- Implement policies that encourage stakeholders to invest more and maintain

business ethics such as announcing incentive scheme packages similar to

those in use in India for - plantation, tea machinery and irrigation equipment,

loan new tea unit, reclamation subsidy, rejuvenation, pruning and consolidation

scheme.

- Prioritize the construction of access roads to tea plantation pockets

identified as high priority

- Implement friendly Labour Act and Regulations

6. SWOT Analysis of Tea

7. World markets

Over the last decade, key features of the tea market have been low prices,

oversupply and in turn, fierce competition. The fall in prices was mainly

caused by high world production due to the expansion of the area under

cultivation and exports. Major tea producers such as Bangladesh, Kenya,

Malawi and Tanzania expanded their tea production area by more than 130,000

hectares in the first half of the 1990s. Prices were also depressed because

of the presence of low quality tea on the market as well as competition

from other drinks. Tea experts are calling for strict quality control

standards to reduce the effect of low quality teas on the market. To counter

the trend of tea loosing ground to soft drinks, the tea industry is actively

trying to promote consumption in the EU and the US by emphasizing the

health benefits of drinking tea compared to coffee. The promotion of ready-to-drink

tea is also being explored as it can compete with soft drinks.

After some signs of recovery in 2004, the FAO composite price for tea

declined by 1.2% to an average of USD 1.64 a kg in 2005.25 Some improvement

in demand eased supply pressure on prices at the start of 2006 when the

composite price peaked at USD 1.92 a kg in February. After some corrections

during the middle of the year, prices strengthened due to weather induced

reductions in supplies in Kenya. (Public Ledger Dec 18, 2006.) China,

Sri Lanka, Kenya, India and Turkey are the largest producers. India and

China are at the same time very large consumers. Sri Lanka is the world’s

largest tea exporter with a 21 percent global export market share. Kenya,

which produces mainly cut, tear, and curl (CTC) tea—used primarily in

tea bags—has a similar market share. About 44% of world production is

CTC tea and 31% Orthodox tea, with green tea making up the balance.

On the demand side Russia is the major market followed by the United Kingdom,

Pakistan, the United States, Japan and Germany. Tastes vary significantly

around the globe. Russian tea drinkers have a distinct preference for

black tea. While the Russian market was initially dominated by Orthodox

tea, the Orthodox tea is shifted to CTC on prices considerations. Recently,

the trend has changed again with CTC demand steadily falling and Orthodox

tea re-emerging as the preferred variety. The price paid for tea also

varies greatly. Germany and Japan prefer First Flush Darjeeling, at more

than USD 30 per kg, while consumers in the UK appear reluctant to pay

even USD 2.50 for top quality Kenyan tea. Consumer tastes differ not only

with regard to quality and origin: continental Europe buys leafy orthodox

teas, while the UK prefers CTC’s more suitable for tea bags. Average CIF

import prices vary significantly between countries, from USD per 3/kg

in Russia (for black tea in packages of less than 3kgs) to USD 12/kg in

Norway and 13/kg in Finland, demonstrating that there is significant scope

for value addition. Orthodox teas can be sold at a better price, especially

when marketed well, as has been done by India with its Darjeeling teas.

However, it is difficult to determine exactly where the markets for orthodox

tea are and how they are performing. Organic certification and other teas

focusing on high quality are further differentiating factors. Nepal’s

market access conditions to all markets, especially in market openness,

is very favorable, but Nepal does not have any tariff advantages. Nepal

enjoys free access in the major markets, with the exception of Russia

that imposes a very high conditional tariff of 20%, with a minimum payment

of 0.8 Euros per kilogram.

Major OECD countries, Russia, and Syria are the most attractive markets

for Nepalese orthodox tea. Nepalese tea is highly underrepresented in

most of the attractive markets. Syria, US, and UK show much higher growth

than the world growth, implying highly dynamic markets. At the regional

level, India is a very attractive market for Nepalese tea, especially,

owing to high tariff advantages as opposed to its competitors.

Conclusion

Like coffee, tea is a cash crop with steady international demand. With

hilly Nepal’s climate and terrain suitable for premium niche product in

the world market, tea has a potential to benefit large segments of rural

population and lift them out of poverty and stagnation.

Growth in the tea sector in Nepal was spurred by the trade liberalization

policies adopted in early 1990s. Since the end of state monopoly in 1993,

numerous tea estates have been established by industrialists and businessmen.

Simultaneously, small farmers have been attracted to growing tea as the

demand and prices for orthodox tea bring higher returns than traditional

crops. As an example, the amount of land used for growing tea has increased

by five times and production has increased by more than 500% compared

to the pre-liberalization figures. More importantly, significant growth

in land use and production both are due to increased participation of

small farmers in producing tea. In numbers, small farmers’ share of the

total land used for growing tea more than doubled in ten years (from 20%

in 1994/95 to 41% in 2003/04). Similarly, small farmers’ share in total

production also rose from 5% in 1994/95 to 33% in 2003/04. Furthermore,

although the numbers vary according to their sources, Nepalese tea sector

directly employs around 105000 people. The beneficiaries of these employees

are many more and are estimated to be around 420000 persons. These are

encouraging figures which suggest an expansive role of this cash crop

is playing in providing Nepalese farmers with alternative to traditional,

low-yield, subsistence farming.

DOWNLOAD

FREE TERM PAPER »

» »